Small Cap Value Report (Fri 22 Mar 2024) - IGP, TRAK, DARK, SYM, BILN, REC, SAG, ECEL

Good morning from Paul!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates amp; results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it’s anybody’s guess what direction market sentiment will take amp; nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed – please be civil, rational, and include the company name/ticker, otherwise people won’t necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we’re not making any predictions about what share prices will do.

Green (thumbs up) – means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it’s such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber – means we don’t have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) – means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we’re not saying the share price will necessarily under-perform, we’re just flagging the high risk.

Links:

Paul amp; Graham’s 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul’s podcasts (weekly summary of SCVRs amp; macro views) – or search on any podcast provider for “Paul Scott small caps” – eg Apple, Spotify.

Other mid-morning movers (with news) -

Trakm8 Holdings (LON:TRAK) - down 36% to 9p (£4.5m) – Profit warning - a large contract negotiation that underpinned FY 3/2024 forecasts is now not going to happen in time. Feb amp; Mar also slower than expected in its insurance-related telematics. New guidance: revs £16.4m and adj loss before tax of £(1.4)m. That’s miles away from last forecast (24/11/2023) from Allenby of £1.8m adj PBT. Cash looks tight at £0.4m, and they forgot to tell us today that they’ve got substantial debt: £5.3m term loan with HSBC, and £1.6m convertible loan (expires 9/2024, 12% interest, 17.1p conversion). I recall TRAK has sailed close to the solvency edge in the past, and it looks pretty much bust now without a placing and/or debt for equity swap – the lenders are probably having kittens and looking for a bail out from equity holders – equity could be worthless, who would want to put in fresh cash to pay off the bank?! Also warns on FY 3/2025 profits. Management have been around a long time, and repeatedly disappointed, so why would anyone believe any new assurances? It’s a RED from me.

Darktrace (LON:DARK) – down 9% to 418p (£2.94bn) – Secondary Placing – remember these are when existing shareholders exit, so no financial effect on the company itself. Full exit of shareholder KKR Dark Aggregator LP – has sold into the recent share price spike (peaked at c.490p on 14/3/2024), 19.4m shares (2.8% of the company) at 425p. Yesterday’s close was 461p. I looked at it briefly here on 7/3/2024 – impressive H1 results with large rise in profits amp; raised future guidance. Doing some googling, I see DARK was attacked by short-sellers last autumn, who will have suffered heavy losses in the recent spike, if they’re still short? Dangerous game shorting, especially if leverage is involved. Or maybe they had previously closed out, having been unsuccessful in trying to trigger a share price crash last autumn? Also it looks as if DARK was previously attacked by shorters in 2022, detailed on Wikipedia here.

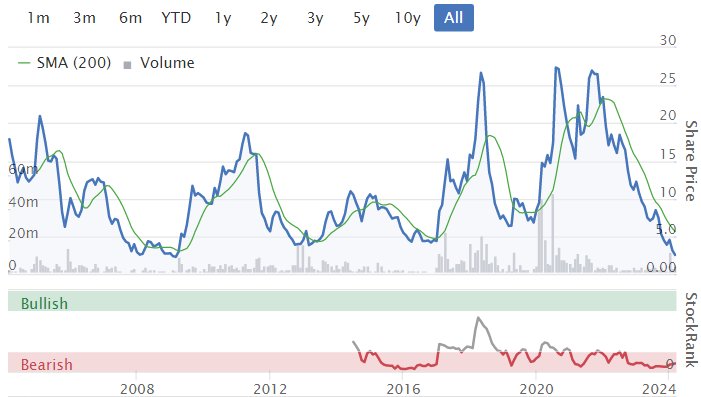

Symphony Environmental Technologies (LON:SYM) - up 31% to 2.75p (£5m) – Fundraise – very small, but I thought this deal looks noteworthy. A serial disappointer, recyclable plastics company. As you can see from the chart below, it’s been around donkey’s years, and every now and then mug punters (including me a couple of times!) chase up the shares on positive-sounding news that fails to turn into profits. Today it announces a small equity fundraise of £1.4m that’s priced at 3.5p, a 67% premium. The money has mainly come from its 2 largest independent shareholders, and the CEO. So they obviously want the share price up, and are backing that with fresh money of their own – I like that. In a long amp; detailed announcement, it says that the shares are undervalued, and that prospects for 2024 are looking better than they have for a while (my summary, to reduce the wordcount!). Another £0.5m is also being offered on Primary Bid. there was some kerfuffle over an EU judgement recently. Balance sheet is fairly weak, and note it has modest debt, and convertible loans from shareholders. So it’s quite encouraging to see them putting in fresh equity this time – which gives credibility to the positive outlook comments below, I think.

I’m tempted to have a fun money punt again, but that has been a mistake in the past. Can mgt assurances be believed though? -

The opportunities for Symphony are significant, and whilst taking considerably longer to convert than originally anticipated, a combination of more positive conversations, trials and other factors give the Board confidence that these can and will be converted in the short to medium term. In the meantime, with the lower cost structure and consistent high gross margins (40 per cent.), the 2024 outlook shows a much more positive commercial position for the Group compared to recent years.

Billington Holdings (LON:BILN) - up 13% to 450p (£58m) – £90m contract awards – Paul – AMBER/GREEN

Structural steel company. We like the numbers for BILN, and were amber/green on 14/11/2023 (ahead exps TU). Good bal sht, decent divi yield. Worries about cyclicality in a downturn seem unfounded given news of 6 new contracts today, a record order book, all “further underpinning” market expectations for 2024 and “into 2025”.

Paul’s opinion – I like BILN, and today’s news bolsters the bull case – although how much is already in the price, given it’s already more than doubled since autumn 2023?

Summaries of main sections

Intercede (LON:IGP) (Paul holds) – up 13% to 112.5p (£66m) – New Orders amp; Trading Update – Paul – GREEN

Another contract win means Cavendish ups FY 3/2024 forecasts (by 4%) for the seventh time since first introduced! I run through the detail below. This remains one of my top 20 share ideas for 2024, and I see scope for further progress.

Record (LON:REC) – down 5% to 63p (£126m) – Trading amp; Business Update – Paul – GREEN

Shares dipped a little today on news of an IT project being abandoned, but the numbers involved seem small to me. More importantly, it’s reached a new all-time high in AuM. I continue to like this share, with a modest valuation, and 8% yield whilst you wait for a re-rating. Maybe I’ve missed something negative?

Science (LON:SAG) – 394p (£179m) – Audited Results FY 12/2023 – Paul – GREEN

Paul’s Section: Intercede (LON:IGP) (Paul holds)

Up 13% to 112.5p (£66m) – New Orders amp; Trading Update – Paul – GREEN

Intercede, the leading cybersecurity software company specialising in digital identities, today announces a new contract win, further strong trading and uplift on market expectations for the current financial year ending 31 March 2024 (“FY24″)*.

* The current market forecast for the year ending 31 March 2024 is revenue of £19.2 million and adjusted EBITDA of £5.6 million.

Key point – IGP prudently doesn’t capitalise Ramp;D spending, so EBITDA actually is a meaningful number here. I’ve told them they should be quoting PBT instead (because it’s a more credible number, and is only slightly below EBITDA for this company), but the analysts prefer EBITDA I believe. Well, at least I tried to help!

Cavendish (many thanks to them) raise FY 3/2024 forecasts c.4% -

Revenue goes from £19.2m to £20.0m

Adj EBITDA from £5.6m to £5.8m

Adj PBT from £5.3m to £5.5m

Adj EPS from 7.4p to 7.7p

Remember that FY 3/2024 benefits from a one-off mega contract. So FY 3/2025 forecasts are more meaningful for valuation purposes. This is £16.1m revenues, £3.0m adj PBT, and adj EPS of 3.7p. Giving a FY 3/2025 PER of 30.4x - but PER is a blunt tool at fast-growing tech companies. They’re often valued on a (quite high) multiple of EBITDA, or even the bonkers multiple of sales ratio, which ignores profitability completely. There’s big operational gearing here due to high gross margin on licence sales, and largely fixed cost base, so each new contract drops through nicely to profit.

Cavendish’s note hints at further upgrades for FY 3/2025 being possibly (likely?), and says it has upgraded FY 3/2024 no less than seven times since forecasts were first introduced. So we now have a very credible pattern of under-promising and over-delivering, which is what we very much like to see here at the SCVR.

Clients are very sticky at IGP, and it has high levels of recurring and repeating revenues. There is single client risk though, as it has some very large contracts that renew every year.

Paul’s opinion – a long-term favourite of mine, it’s great to see Intercede on a roll now.

I’ve invited the CEO to do an interview on my podcast channel, maybe after the next results are out? It’s one of my top 20 share ideas for 2024, so these upgrades are helping my performance stats! Although Graham remains stubbornly 1% ahead of me, not that we’re competitive ![]()

In my experience, once companies start winning a flurry of decent contracts, it usually continues, although I can’t back that up with any firm data. Especially when they’re won through channel partners, who gain confidence in solutions that work and then might put Intercede forward as their preferred choice on future deals. Remember that IGP software is for managing secure user credentials, so it’s a cog in a bigger machine of IT systems.

Overall I’m happy to remain at GREEN, and I don’t see £66m market cap as being anywhere near stretched given the growth, and the potential, and the stunning client list that includes multiple US Federal Govt departments, major aerospace companies, banks, etc.

For full disclosure, I’m a shareholder personally, and intend sitting tight/adding more on dips if funds are available.

5-year chart below shows how quickly shares like this can rise when a flurry of good newsflow happens, blink and you miss it. I see this as probably a sustainable rise, because it’s backed by big contract wins and forecast upgrades -

Look at the scale of the large one-off contract win on FY 3/2024 forecasts below. Although remember each big contract typically comes with a multi-year tail of support amp; upgrade revenues -

Record (LON:REC)

Down 5% to 63p (£126m) – Trading amp; Business Update – Paul – GREEN

Record plc (“Record”, the “Company” or the “Group”), the specialist currency and asset manager, announces a trading and business update for the year ending 31 March 2024 (“FY-24″).

Assets under management equivalent has hit a new all-time high of $101.3bn at 29/2/2024.

FY 3/2024 revenues expected to be £45m, in line with market expectations.

Abandoning a 2-year IT project via external consultants, to focus on internal IT instead.

Costs don’t seem significant at £0.5m restructuring, and £1.9m write-off intangibles.

Paul’s view – assuming this update is giving us the full picture, it doesn’t sound like anything to worry about, abandoning a smallish IT project, these things happen.

I remain of the view REC looks an attractive niche business, and EPS has gone up a lot in recent years. The dividend yield is seriously good, at c.8% after today’s drop in share price. Is it sustainable? I think it should be, as this is a capital-light business that pays out most of its earnings as divis each year. Maybe I’ve missed something, as the share price seems to be in a downtrend? Providing nothing goes wrong, patient investors could enjoy a re-rating of this share at some stage, and get paid an 8% dividend yield whilst you wait. Management changes in progress.

Science (LON:SAG)

394p (£179m) – Audited Results FY 12/2023 – Paul – GREEN

Figures were published yesterday. I’m coming back to these as we like SAG here at the SCVR, viewing it as GREEN on both 24/7/2023 (H1 Results), and 22/11/2023 – in line TU.

Figures for FY 12/2023 look good -

Revenue up 31% to £113.3m

Adj operating profit up 16% to £20.5m

PBT is close to operating profit, given that net finance costs are only £526k

Adj EPS up 13% to 33.3p (PER 11.8x)

Diluted statutory EPS is much lower, at 12.0p, so make sure you’re happy with the adjustments, as they’re big, and include a rather generous £2.0m share based payment charge.

Balance sheet is sound I think, with £33m NTAV. Includes £31m of cash, partially offset with £13m of bank borrowings. Note freehold properties are valued at cost of £20.6m, with a open market valuation of a rather bizarrely wide range between £16.9m to £31.6m! Surely commercial property can be valued more accurately than that?

The core consultancy businesses, which generate most of the profit. Then it also has an audio chips business, Frontier, and a submarine related business.

Frontier had a bad year in 2023 (previously mentioned in the H1 results) with a “small operating loss”, but new product development was all expensed through the Pamp;L. It says Frontier should perform better in 2024, helped by improving market conditions and cost cutting.

Acquisition of TP Group sounds like it’s going to plan.

Divis amp; buybacks continuing.

The Exec Chair has this (below) to say in conclusion. It’s not clear to me what he’s hinting at here? Inviting takeover approaches, taking it private, inability to issue new equity for acquisitions at an attractive price vs cost of acquisitions? Who knows -

For over a decade, Science Group has demonstrated a consistent operating track record, enhanced by a successful Mamp;A programme, delivering a substantial return for shareholders. While the Group has the ambition and capability to accelerate the strategy, the relative valuation of the company against both UK and international comparators may prove a material constraint. The Board will therefore consider all options to address this disparity and deliver value to shareholders.

Paul’s opinion – remains positive. SAG seems to have absorbed the sharp fall in profits at Frontier through its other businesses performing well, and an acquisition.

Maybe the lowish rating on the shares is because SAG seems a strange hotch-potch of different businesses?

It’s effectively owner-managed, with the Exec Chair owning 20.7%, and 5 institutions owning c.50% of the group. So he would only need to make 5 phone calls to get any kind of deal done.

I’m wondering if a takeover bid might come along for SAG? Maybe that’s what the Chairman is hinting at above? Anyway, the shares look pretty good to me, so I’ll happily stick at GREEN.

Holding on to most of the 2021 gains is a good performance relative to many other small cap shares. High StockRank too -

Eurocell (LON:ECEL)

116p (£127m) – Preliminary Results FY 12/2023 – Paul – GREEN

Eurocell plc, the market leading, vertically integrated UK manufacturer, distributor and recycler of innovative window, door and roofline PVC products, today announces its preliminary results for the year ended 31 December 2023.

This was on my top 20 list for 2024, hoping for a cyclical recovery to start, and underpinned by a strong balance sheet. The idea being that it would then just be a case of waiting for a recovery to start. It hasn’t worked so far, but it’s early days.

Here’s a nice summary from the company -

Revenue down 4% to £365m

Adj PBT down 55% to £15.2m

Adj basic EPS down 49% to 11.0p

They nearly caught me out, by switching from % to absolute amount in the change column. So I had to work out my own percentages above (apart from revenue). Sneaky.

Net cash of £0.4m (LY: net debt of £(14.4)m)

Not a good year then in 2023, but we already knew that, and it’s why the share price is still bombed out, and forecasts have fallen a lot -

Margin pressure is a concern -

Increased competition for limited demand leading to pressure on margins in the branch network

Divis almost halved compared with 2022. Share buyback of £5m is half completed so far.

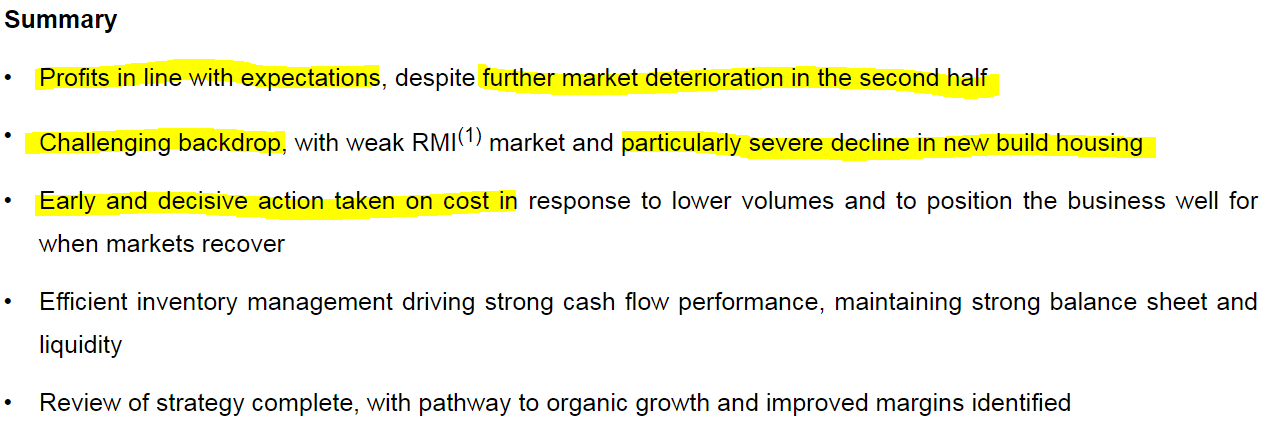

Outlook – are they seeing any green shoots yet? Not really, no -

Whilst the near-term outlook for our markets remains challenging, these actions leave us well placed to benefit from a market recovery when it comes.

Our review of strategy is now complete and I am very pleased with the outcome. Looking ahead, we have identified a clear pathway to building a £500m revenue business, generating a 10% operating margin over a five-year period…

Let’s not run before we can walk!

Balance sheet looks very nice, with NTAV of £98m, supporting most of the £127m market cap. No bank debt to worry about, although I imagine it would use a bit of bank debt from time to time in normal daily operations.

Cashflow – is very impressive, even when you adjust for the lease finance charges distorting the numbers.

Paul’s opinion - I’m very comfortable with ECEL, as a securely financed business that has remained profitable even in tough market conditions. Recovery? It should happen at some point, hopefully.

Source: https://www.stockopedia.com/content/small-cap-value-report-fri-22-mar-2024-igp-trak-dark-sym-biln-rec-sag-ecel-992939/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Please Help Support BeforeitsNews by trying our Natural Health Products below!

Order by Phone at 888-809-8385 or online at https://mitocopper.com M - F 9am to 5pm EST

Order by Phone at 866-388-7003 or online at https://www.herbanomic.com M - F 9am to 5pm EST

Order by Phone at 866-388-7003 or online at https://www.herbanomics.com M - F 9am to 5pm EST

Humic & Fulvic Trace Minerals Complex - Nature's most important supplement! Vivid Dreams again!

HNEX HydroNano EXtracellular Water - Improve immune system health and reduce inflammation.

Ultimate Clinical Potency Curcumin - Natural pain relief, reduce inflammation and so much more.

MitoCopper - Bioavailable Copper destroys pathogens and gives you more energy. (See Blood Video)

Oxy Powder - Natural Colon Cleanser! Cleans out toxic buildup with oxygen!

Nascent Iodine - Promotes detoxification, mental focus and thyroid health.

Smart Meter Cover - Reduces Smart Meter radiation by 96%! (See Video).

| Online: | |

| Visits: | 1,604,509,166 |

| Stories: | 8,153,472 |

Whistler Blowers, Insiders